Q4 2026 Earnings Call Transcript")

")

Due to the educational nature of this article, I won’t be rating the NEOS Bitcoin High Income ETF (BTCI). Instead, I’ll break it down into its individual parts so it’s easier to understand.

What’s BTCI Made Of?

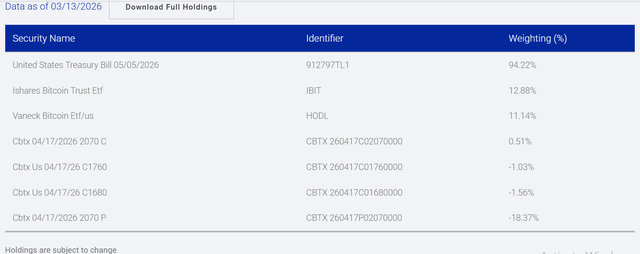

The prime directives of this ETF are distributions and price capture using indirect and synthetic exposure to Bitcoin (BTC-USD) with covered call selling. The indirect exposure comes from holding spot bitcoin funds like the iShares Bitcoin Trust ETF (IBIT) and the VanEck Bitcoin ETF (HODL), a long position is created by buying calls and selling puts at the same strike and expiration on bitcoin-adjacent instruments, and calls are then sold on this synthetic long position to collect premiums. This scaffolding, or laddering, is constructed with the following holdings (as I write this).

NEOS

The holdings are broken down to 94% cash, 24% in iShares and VanEck spot Bitcoin ETFs for the indirect exposure, the call-put synthetic long position, and the covered call selling (at the time of writing). The options positions roll over periodically, and on and on it goes. The fund has been around for about a year and a half, with an inception date of October 16, 2024.

BTCI’s expense ratio is 0.98% net of AFFE or acquired fund fees and expenses, and in the 1.5 years it’s been with us, the AUM has grown to over $960 million. The yield on the dividends current runs at a trailing figure of 43%.

Historical Performance

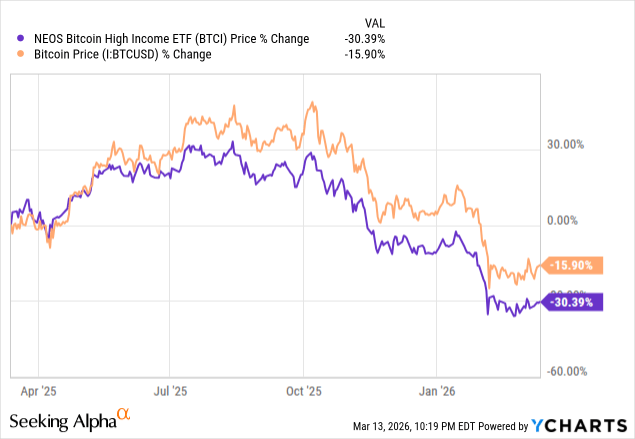

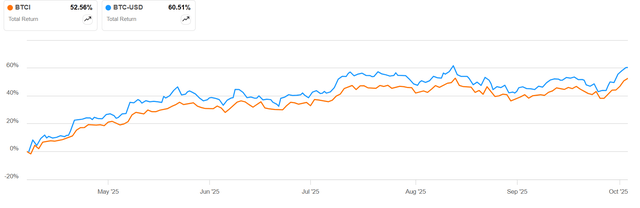

Since the fund is indirectly exposed to Bitcoin, it’s not really a surprise that it somewhat tracks the price of the underlying asset. Since this is a high income strategy reliant on covered calls, that comes at the cost of price underperformance — your cow gets thinner the more you milk it. In the last the 1Y period, you can see how bitcoin’s been struggling for more than half that time.

There’s a concept called path dependency that’s useful to know about with regard to income ETFs that rely on income generated from options premiums. The effect of path dependency is linked to the expiration of the options contracts. Funds like BTCI that hold one-month-forward contracts are essentially locked out for that period because they can’t fully participate in rallies that are shorter than a month. When the underlying asset experiences a downturn, the BTCI’s NAV also draws down similarly. Then, there’s less “cow” on which to write these options contracts in the future for the “milk.”

An even more detrimental effect is asset value drag, and this is tied to the moneyness of the strikes. Far OTM strikes may work better here because there’s less of a lockout, but the fund needs to find an ideal balance because near-the-money calls have higher premiums, and this is key to stabilizing the monthly income. In a prolonged bear market, if the fund wants to maintain its payouts, that cow is going to get thinner a lot faster.

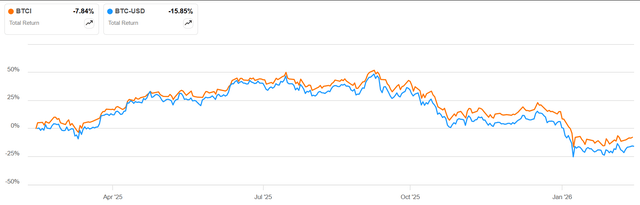

I’m not building a case for or against BTCI, as I said, so you’ll need to balance this view with a look at total return because it’s actually done much better than bitcoin. One important point of note here is that TR is always based on dividends being reinvested, which doesn’t really make sense for an income ETF. Still, a cash payout is a type of return even though it may reduce the fund’s net assets and therefore reduce your TR moving forward.

SA

What’s happening is that the income that BTCI is generating through its synthetic covered call selling strategy has given it an advantage over a pure crypto holding, even after paying the gross ER of ~0.99%. Since you’re taking out the cash every month, your TR should theoretically approximate what you’d get from a pure play bitcoin holding.

Pros and Cons

You’ve got a unique way to convert a synthetic bitcoin position into cash, and it’s all because of the way the portfolio is constructed. You’ve got your upside from the fund holding spot bitcoin ETFs, and there’s a tax benefit that we’ll be discussing below.

Don’t mistake those pretty big advantages for the absence of negatives, because there’s plenty of that. In this section, let’s look at the pros and cons, and how it helps on the taxation side of things.

I’m hoping this gives you a balanced view of BTCI so you can begin your own investigation into this cash generator. I’d also like to comment on the tax treatment for the distributions because that’s an important piece of information when you’re looking at the feasibility of investing in the ETF.

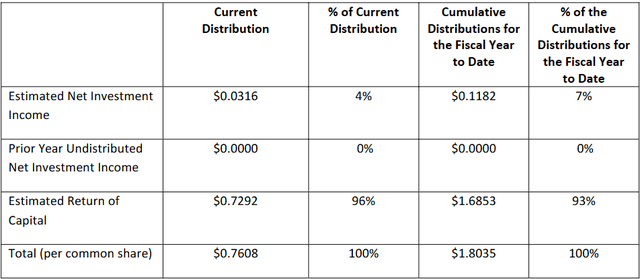

If you look at the 19a-1 notices for each month, like the one for February 2026, you’ll notice that most of it is being returned as capital.

NEOS

While the 19a is an approximation of tax treatment giving investors a monthly idea of what to expect, the end of year tax statements and documents like Form 8937 has the final breakdown. That’s the tax treatment angle, and it’s important to know how that will affect what you pay the taxes.

Normal dividend income is typically treated as ordinary income for the purpose of taxation. Depending on your tax bracket and a whole bunch of other considerations, you’ll end up paying a higher rate than what you’d pay on capital gains.

Now, the fund wants to pay you a hefty dividend every month, and that cash has to come from somewhere, right? We know it’s generated by contract premiums, but by accounting for it as a return of your invested capital most of the time (RoC), the fund helps you cut your present tax burden considerably. The IRS treats this as your own money coming back to you, which means the cost of the investment you first made comes down by that much. The real kicker is that you can defer your taxes until you sell that position, and it helps the longer you hold it because the capital pile keeps getting smaller, and your tax on that tapers down in lockstep. However, once you reach your cost basis of 0%, gains above this are treated as long-term capital gains. Talk to your tax professional for more clarity on your own tax position, but that’s the short lay version.

There’s also a problem that goes with it. We saw the flip side as the fund being unable to take advantage fully of bitcoin price escalations, and if you look at the period last year where bitcoin had a 60% run-up, that’s obvious.

SA

Key Takeaways

Incidentally, just this past week, the 20 millionth bitcoin was mined, theoretically giving us 114 years before the final millionth is mined into existence. The future may look good for Bitcoin. Most experts, including Grayscale, say that 2026 will be a pivotal year for two reasons — the demand for a non-conventional store of value, and regulatory integration of bitcoin into the mainstream economy. Time will tell.

There’s plenty to like about BTCI, and equally, lots to be wary of. If you want direct exposure to Bitcoin, investing in BTC-USD or a spot bitcoin ETF may be the better route. Conversely, if you’re looking for income that helps take away some of your present tax load, this might be the right vehicle for the job.

Suitability

A few final points before I go. This ETF isn’t for everyone. It’s designed for a specific type of investor who’s willing to let some upside go so they can enjoy ongoing income. The payouts are really attractive, the return of capital is good for tax purposes, and you’re taking advantage of bitcoin’s price movements so you’re a participant in at least some of the upside. The other side of this coin is that you don’t get full exposure to strong bitcoin rallies, you don’t really own any of the underlying assets, but you still run the risk of sharp or prolonged drawdowns decimating the asset base that’s printing that cash for you. This may be a useful ETF for those who anticipate a sideways market and foresee the total return profile of BTCI may be more attractive than straight Bitcoin for a period of time.

How you use it as part of your portfolio strategy is what ultimately matters, but I hope I’ve been able to shed enough light on BTCI for you to use as a starting point for your own scrutiny.

This article answers three questions about BTCI:

- How does BTCI relate to the price of Bitcoin?

- What risks should investors consider when owning BTCI?

- Which environments and investor types is BTCI best suited for?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Read the full article here

")

")